TL;DR

Fake medical bills are more common than most people think and they cost patients, insurers, and healthcare providers billions every year. If you’ve received a medical bill that looks off, there are specific things to check: provider details, itemised charges, duplicate line items, and whether the bill has a verifiable authentication mark. This article walks you through exactly how to spot a fake, and what healthcare providers can do to make sure their own billing documents cannot be forged using QR Code verification.

According to the National Health Care Anti-Fraud Association(NHCAA), healthcare fraud costs the United States over $68 billion annually, with fraudulent billing among the most common schemes.

With the rise of AI and editing softwares, faking a medical bill has become easy. Therefore, for hospitals it becomes important to use a strong verification layer. There are many editing softwares available online providing free medical bill templates that make it very easy to forge a medical bill.

For hospitals, this is a sign to make their security strong. Today, we’ll be learning more about it.

I will walk you through what fake medical bills are, how they are faked, and practical solutions for hospitals to protect their issued medical bills from forgery. So, keep reading till the end!

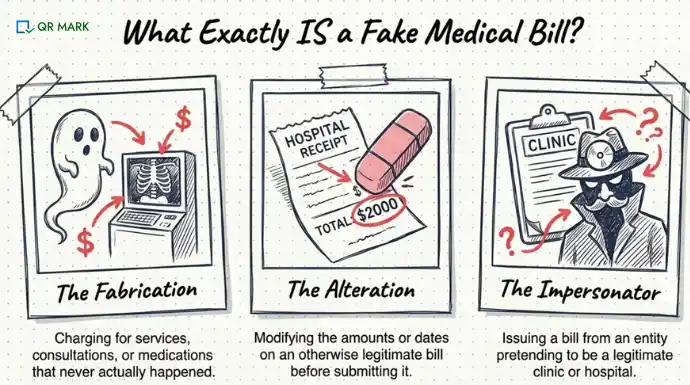

What is a fake medical bill?

A fake medical bill is a billing document that misrepresents medical services either completely fabricated, altered from a real bill, or issued by someone impersonating a legitimate healthcare provider.

Here’s a simple way to think about it: if you were charged $800 for an X-ray you never had, or if someone changed the amount on your original hospital receipt from $200 to $2,000 before submitting it to insurance, both of those are fake medical bills.

Example: A patient receives a bill from “City General Hospital” for an emergency room visit on 14 March. The visit happened, but the bill charges for a CT scan, two specialist consultations, and medications — none of which were actually administered. The document looks real. It has a logo, a patient ID, and an itemised list. The only thing that’s fake is most of the content.

This type of fraud can be run by external bad actors, but it’s also done internally, by healthcare staff, billing departments, or third-party billing companies manipulating records for financial gain.

What makes a medical bill fake?

Most fake medical bills share the same set of problems. Once you know what to look for, the signs are hard to miss.

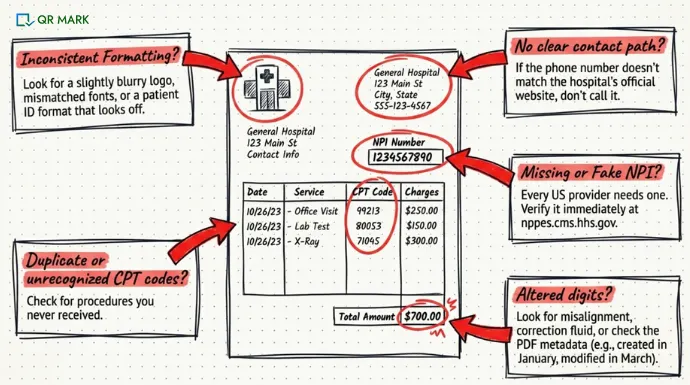

The provider information doesn’t check out

A legitimate hospital or clinic has a verifiable address, phone number, and NPI (National Provider Identifier) number.

If any of these are missing, wrong, or lead nowhere when you search them, that’s a red flag.

You can verify any US healthcare provider’s NPI at nppes.cms.hhs.gov.

The charges don’t match your care

Every service on a medical bill has a CPT (Current Procedural Terminology) code. If you’re being charged for a procedure, that code should match what actually happened during your visit.

Fake bills often include codes for services that weren’t performed, or duplicate the same service multiple times under slightly different descriptions.

The dates or amounts have been altered

Physical bills that have been tampered with sometimes show signs of correction fluid, inconsistent font sizes, or slight misalignment in the text.

Digital bills edited in PDF software sometimes have different fonts within the same document, or metadata that doesn’t match the stated issue date.

There’s no way to verify it

A bill from a reputable provider should come with enough information for you or your insurer to confirm it’s genuine.

If there’s no contact path back to the issuing provider, or if the contact details differ from the provider’s official website, something is wrong.

The formatting is inconsistent

Logo quality, address formatting, and document layout tend to be standardized within a hospital system.

Fake bills often get the details right but miss small things: a different font in the header, a logo that’s slightly blurry, or a patient ID format that doesn’t match other bills from the same provider.

How do you spot a fake medical bill?

Go through this in order. Each step takes less than five minutes.

- Cross-reference the provider’s contact details. Search the hospital or clinic name independently — don’t use the phone number printed on the bill. Call the number you find on their official website and confirm the bill was issued by them.

- Check the NPI number. Every legitimate US healthcare provider has an NPI. Search it at nppes.cms.hhs.gov. If the NPI doesn’t match the provider name on the bill, it’s not a real bill from that provider.

- Request an itemised bill. If you receive a summary bill, ask for the full itemised version. Every charge should have a CPT code. Look for duplicates, services you don’t recognise, or charges that seem disproportionately large relative to the service described.

- Match it against your Explanation of Benefits (EOB). If you’re insured, your insurer sends an EOB for every claim processed. The services and amounts on the bill should match your EOB. If they don’t align, either the bill or the claim has been manipulated.

- Check the document metadata. If you have a PDF, open the file properties. Look at the “created” and “modified” dates. If a bill dated January was last modified in March, it’s likely to be edited after the fact.

- Look for a verification mark. Some healthcare providers now embed QR Codes or digital verification into their billing documents. If a bill has one, scan it. If the verification fails or the QR Code leads to a broken or suspicious page, the document has been tampered with.

Most fake bills fail at step one or two. Legitimate providers are easy to verify. Fake ones aren’t.

What should you do if you discover a fake medical bill?

Don’t pay it, and don’t ignore it. A fraudulent bill that goes uncontested can end up in collections, damage your credit, and become significantly harder to dispute later.

Work through this in order:

1. Contact the provider directly not using the number on the bill

Look up the hospital or clinic on their official website and call that number. Ask them to confirm whether the bill was issued by their office. If they have no record of it, you have your answer.

If you discover that the document has QR Mark’s code in it. Scan it and report fraud directly. Simply add the issue, add your email address and your report will be sent to the issuer directly. This will save you a lot of time.

P. S – If you are a healthcare provider and want to introduce a system like this, you can try QR Mark for free!

2. Notify your insurer

If the bill has already been submitted to your insurance company, alert them immediately. Insurers have fraud investigation units filing a report with them triggers a formal review and stops reimbursement from being paid out on a fraudulent claim.

3. File a report with the FTC

In the United States, healthcare billing fraud is reportable at reportfraud.ftc.gov. Your state insurance commissioner’s office is a second avenue, they have jurisdiction over fraudulent billing within their state.

4. Dispute any collections activity

If the bill has already been sent to a collections agency, dispute it in writing with the agency and request verification of the debt. File a dispute with the credit bureaus if it has appeared on your credit report.

5. Keep everything

The bill, the envelope it arrived in, any emails or calls related to it, and any correspondence with the provider or insurer. Documentation is what makes a fraud report actionable.

What should a healthcare organisation do if its billing documents are being forged?

If patients, insurers, or employers are receiving fraudulent bills in your organisation’s name, the damage is twofold: financial and reputational.

Patients who are defrauded using your logo and provider name lose trust in you, even though you’re also a victim.

Acknowledge it publicly if the volume warrants it

If you’re receiving multiple reports of forged bills circulating under your name, issue a notice on your website and patient portal explaining what legitimate bills from your organisation look like and how to verify them. Silence looks like complicity.

Report it to law enforcement

Healthcare fraud involving impersonation of a provider is a federal crime. File a report with the FBI’s Internet Crime Complaint Center (IC3) and notify your state’s healthcare fraud unit. Your legal team should also assess exposure under HIPAA if patient data appears on the forgeries.

Audit your billing workflow

Forged bills that closely replicate your real invoices like correct logo, accurate provider address, plausible CPT codes often indicate that someone has access to a genuine bill. Review who has access to billing documents and whether any have been leaked through a third-party billing company.

Make your legitimate bills verifiable

The most durable fix is structural: if every bill you issue carries a scannable verification mark linked to a record on your own domain, any recipient can confirm authenticity in seconds and any forged version immediately fails that check.

This removes the confusion that makes the fraud viable in the first place. Tools like QR Mark embed a verification QR Code into each invoice at the point of issue, giving patients, insurers, and employers a direct line back to your records.

What are the practical solutions to prevent medical bills from being faked?

If you’re a patient, the steps above protect you. But if you’re a healthcare provider, a medical billing company, or a hospital administrator, the question is different: how do you make your billing documents impossible to forge in the first place?

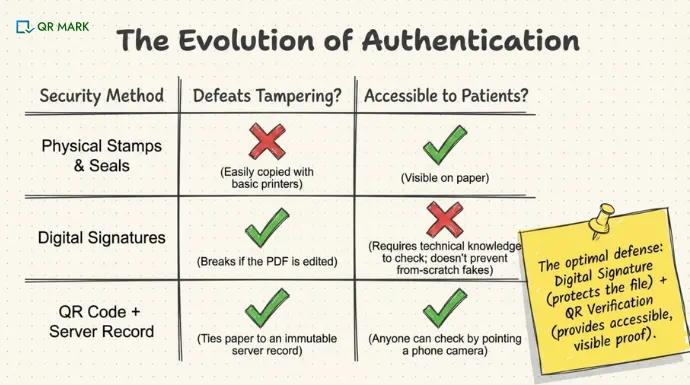

There are three layers that matter here: physical stamps, digital signatures, and QR Code verification. Each does a different job.

Physical stamps were the traditional answer. An embossed stamp or a wet seal on a document made it harder to reproduce.

The problem is that stamps can be replicated with a basic printer and some rubber. They worked when document fraud required physical access and specialist tools. Now they don’t.

Digital signatures are a step up. A digitally signed PDF contains a cryptographic signature tied to the issuer’s certificate.

If anyone modifies the document after signing, the signature breaks and the file shows as invalid in Adobe Reader or any PDF viewer. This is genuinely useful but it has two gaps.

First, the recipient needs to know to check the signature status, and most people don’t. Second, a fraudster can simply re-create the document from scratch without the signature, and the recipient has no way to know a signature should have been there.

QR Code verification solves the second gap. When a QR Code is embedded in a medical bill and linked to a server-side verification record, the document becomes two-sided: the paper (or PDF) and the live record that confirms it.

How do QR Codes help protect the authenticity of medical bills?

When a healthcare provider embeds a QR Code into a billing document using a platform(like QR Mark), here’s what happens:

The provider creates or uploads the bill. The platform generates a unique verification record for that specific document and embeds a QR Code linked to that record.

The QR Code leads to a verification page hosted on the provider’s own domain, not a generic URL.

When a patient, insurer, or employer scans the code, they land on a page that shows: the provider’s name, the document type, the issue date, and confirmation that the document is authentic.

If the bill has been altered in any way, the verification page either won’t load or will show a mismatch.

This is why the domain matters. If the verification page lives at something like verify.citygeneralhospital.com, it’s controlled by the hospital.

A fraudster can’t replicate that. If the URL is a generic third-party domain, a forger could potentially set up a fake verification page on a similar-looking URL which is exactly what QR Mark’s Custom Domain feature is designed to prevent.

How to stop Fake Medical Bills from circulation?

For healthcare organizations, combining digital signatures with QR Code based verification provides a practical and scalable way to protect billing documents from forgery and ensure authenticity.

If you have any further questions, ask in the comments section. I’’ll be happy to help.

Frequently Asked Questions

Can a fake medical bill affect my credit score?

Yes. If a fraudulent bill goes to collections without your knowledge, it can appear on your credit report. Dispute any unknown medical collections immediately with the credit bureau and request verification of the debt.

What should I do if I receive a fake medical bill?

Don’t pay it. Contact the provider listed on the bill using contact details from their official website, not from the document itself. If the provider confirms they didn’t issue the bill, report it to your state insurance commissioner and the FTC at reportfraud.ftc.gov.

Can insurers detect fake medical bills?

Insurers have claims review teams and fraud detection software, but they can’t catch everything — especially when the fraudulent bill closely matches the patient’s actual visit. Embedded verification marks give insurers a faster, more reliable check.

Is it illegal to submit a fake medical bill to insurance?

Yes. Healthcare fraud is a federal crime in the United States. Under 18 U.S.C. § 1347, submitting false claims to a federal healthcare program carries penalties including fines and up to 10 years in prison.

Do I need an app to verify a QR Code on a medical bill?

No. Any smartphone camera app can scan a QR Code. The verification page opens in a browser — no additional software required.