TL;DR

Insurance fraud costs the global industry over $80 billion every year, and most of it starts with a forged or altered document. Not every fraud prevention tool solves the same problem. This article explains what an insurance fraud solution really is, why protection should start at document issuance, how to compare tools before buying, includes a side-by-side comparison of six leading solutions, and provides a step-by-step guide to verifying insurance documents instantly using QR Mark.

Recently in the U.S. in March 2026, I came across a case where a couple running an insurance brokerage pleaded guilty to defrauding clients of over $750,000.

To keep the scheme going, they issued certificates that looked completely real. And honestly, that’s the scary part, there was no simple way for clients or partners to verify them instantly. By the time the truth came out, the money was already gone.

To me, this clearly shows the gap fraudsters take advantage of. When documents can’t be verified easily, people are forced to trust what they see and that’s where things fall apart

The real need is for an insurance fraud solution that ensures every document can be verified the moment it is used.

In this guide, you’ll learn:

- What an insurance fraud solution is

- How to compare insurance fraud solutions based on real-world needs

- A detailed comparison of six leading solutions in 2026

- How to use QR Mark to make your insurance documents instantly verifiable

What is an Insurance Fraud Solution?

An insurance fraud solution protects insurers at both issuance and verification stages by detecting fake, altered, or forged documents before claims are paid.

According to the Coalition Against Insurance Fraud, insurance fraud costs insurers an estimated $308.6 billion annually worldwide, with a large portion of fraudulent claims involving falsified or altered documentation to support bogus claims (2026).

A large chunk of fraud in the insurance sector happens due to submission of fake proofs of insurance, false claims, altered documents, forged policy papers etc..

These include documents such as:

- Policy certificate

- Policy schedule

- Endorsement documents

- Proposal form

- KYC documents (ID & address proof records)

- Risk assessment reports

Why Should You Secure Insurance Documents at the Point of Issuance?

The best place to stop insurance fraud is when the document is created, not when the claim is filed.

Once a policy certificate or document is issued, it starts moving across customers, hospitals, garages, and agents. If it isn’t secured at that point, it can be edited or misused — and anyone handling it can alter it without a trace.

Securing at the point of issuance changes the dynamic:

- Anyone handling the document can instantly check if it is real, without relying on how it looks

- Your team doesn’t have to spend time manually investigating mismatches or chasing verification from third parties

- Claims decisions happen faster when there’s no doubt about a document’s authenticity, genuine claims settle quickly and fraudulent ones are blocked early

You settle genuine claims quickly and block the wrong ones early, in turn, protecting both your customer experience and your bottom line.

How Do You Compare Insurance Fraud Solution Tools Before Choosing One?

Before you evaluate any insurance fraud solution for your company, align on the parameters that actually matter for your use case. Here is how to structure the comparison:

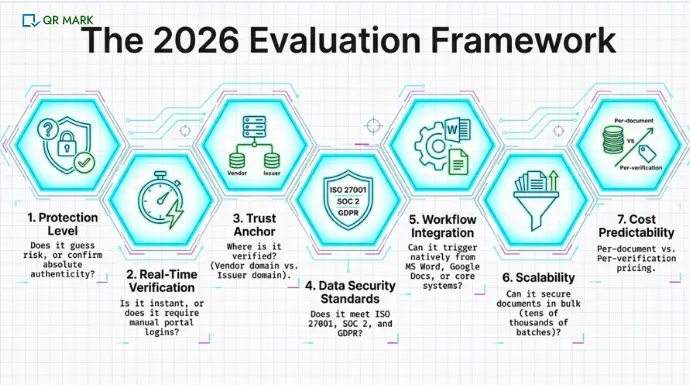

1. What Level of Protection Does This Tool Offer?

There are two fundamentally different things a tool can do: check whether a document looks suspicious based on patterns and signals, or confirm whether the document is genuine based on its original issuance record.

If your problem is fraudulent hospital bills, forged discharge summaries, or fake invoices — a risk scoring tool will not catch those. You need a tool that can help confirm the authenticity of the document at source.

2. Does It Support Real-Time Verification?

Ask how the tool actually helps in verification. Some tools require a portal login every time. Some need a dedicated app.

The best solution should support verification in no-time — no login, no app, no friction.

Make your documents instantly verifiable with QR Mark.

3. What Is the Trust Anchor?

Your aim should be to choose an authenticity solution that has some trust anchor to it.

A trust anchor is the element that reassures the verifier they are validating the document directly with the issuing organisation — not a third party, and not a spoofed page.

For example, if you are using QR Mark, the QR Code will have two trust anchors:

1- Your branding on the QR Code Frame.

2- Whenever, someone will scan the QR Code – it will redirect to a verification page that will be hosted on your domain.

4. What Data Security Standards Does It Carry?

Think about what is on a typical motor insurance claim form — policyholder details, claims history, repair cost breakdowns, sometimes medical reports. A lot of it is sensitive, and a lot of it is irrelevant to the verifier.

Look for tools certified to ISO 27001, SOC 2, and GDPR. These certifications mean the vendor has been audited against recognised standards — and that you can control exactly what data is visible during verification.

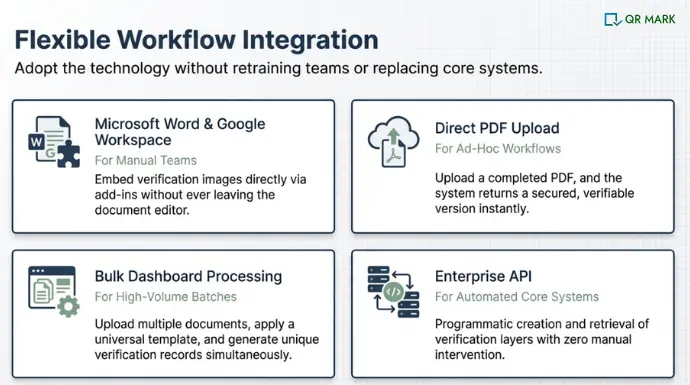

5. Does It Fit Into Your Existing Workflow?

Here is something I have seen tripping up organisations repeatedly: they buy a strong tool and then nobody uses it because it doesn’t fit how work actually gets done.

Insurance documents are created in everyday tools — Microsoft Word, Google Docs, internal policy administration systems. Any security layer that integrates into these workflows is a significant advantage over tools that require a separate process.

For organisations running documents through policy administration platforms or claims management systems, a straightforward API call that triggers the verification layer automatically at document generation is the right approach.

6. Can It Scale to Your Document Volumes?

A large insurer running renewal cycles may issue tens of thousands of policy schedules in a single batch. Ask whether the tool can secure documents in bulk — not just one at a time. Bulk processing capability is the difference between a tool that works in production and one that creates a new bottleneck.

7. Is the Cost Model Predictable at Your Volume?

Some tools charge per document secured. Some charge per verification check. For most insurers and TPAs, per-document pricing is easier to forecast — you tie cost directly to issuance volume.

Before any pricing conversation, calculate your own numbers: how many documents does your network issue per month, and how many get verified? Run those figures through each pricing model before deciding which makes sense for your operation.

What are the best tools to prevent insurance fraud in 2026?

Below is a comparison of six fraud prevention tools, evaluated on the parameters above.

1. QR Code-Based Document Authentication

QR Code based Insurance document authentication secures a document by embedding a dynamic QR code at the time of issuance. That code is linked to a secure backend record created at document generation.

Key document details are stored in the system at that moment. When someone scans the QR Code, they are directed to a verification page hosted on the issuer’s own custom domain. The verifier matches the details on the page against the document in hand.

Example: QR Mark

“Insurance fraud often starts with a document that appears genuine but has been altered or forged after issuance. With QR Mark, insurance companies can issue secure, verifiable documents right at the source. Features like custom domain verification pages, template-based field visibility, API-triggered bulk issuance, and compatibility with Word, Google Docs, and PDF workflows make it easy for insurers to embed security seamlessly into their document creation process protecting both their business and policyholders from fraud.” — Srijan, Head of Product Development at QR Mark

2. Blockchain-Based Document Anchoring

Blockchain-based security registers a document’s digital fingerprint at issuance. During verification, the document is re-hashed and compared against the original record — a hash match confirms the document is unchanged.

But on real-time verification, it requires custom enterprise API integration — not a phone camera scan. Workflow fit is limited to organisations that can support significant technical implementation. Cost ($25,000–$150,000+ annually) makes it viable only for large carriers, not TPAs or mid-market insurers.

Example: IBM

3. Enterprise Document Vault (DMS)

This approach stores documents in a controlled repository immediately after creation. The stored version becomes the authoritative copy. Access controls restrict who can view or edit, and every action is logged.

It’s strong for internal audit trails — but it doesn’t give external verifiers (claims adjusters, hospitals, garages) a self-serve way to check a document in the field. Real-time verification for external parties is limited. Workflow integration requires ERP/CMS connectivity. Cost ($20,000–$100,000+ annually) reflects enterprise positioning.

Example: OpenText

4. Certificate-Sealed Digital Documents (PKI)

PKI-based security applies a cryptographic certificate to a document when finalised. This binds the file to the issuing organisation and invalidates the certificate if content is edited after sealing.

On workflow, Adobe Acrobat integrates natively with Microsoft 365 and Google Workspace. The limitation is verification — recipients must check the certificate status in compatible software. Verifiers in the field (garages, hospitals) are unlikely to have the tools or training to do this reliably. Trust anchor is the Certificate Authority, not the issuer’s own domain.

Example: Adobe Acrobat Digital Certificates

5. Physical Anti-Counterfeit Printing

Physical anti-counterfeit methods embed security features — holograms, microtext, watermarks, UV-reactive ink — directly into the printed document during production.

This is effective for printed formats where visual inspection is part of the verification process. The critical limitation: once the document is scanned and shared digitally, physical protections provide no defence. In an environment where insurance documents routinely arrive as PDFs or photos on a smartphone, this approach loses most of its value at the digital transmission stage. No real-time verification capability. No workflow integration.

Example: De La Rue

6. Direct Source Validation via API

This model validates document data directly from the source system instead of relying on the physical document. When a provider generates an invoice or report, data is transmitted to the insurer through a system-to-system API connection.

On real-time verification and workflow, it’s limited to networks where both sides have integrated systems. Scaling across fragmented provider ecosystems is complex and resource-intensive. Cost ($100,000–$500,000+ annually) reflects the implementation requirement.

Example: Guidewire Software

How do you use QR Mark to prevent insurance document fraud?

Here is the step-by-step process for how insurance companies can make their documents easy to verify with QR Mark:

Step 1: Sign in to your account

- Go to QR Mark.com and log in to your account.

- If you’re new, create an account to get started.

Step 2: Add your custom domain

- Add your custom domain (for example, verify.yourinsurancecompany.com).

This ensures that every policy verification happens on your official domain, building trust with customers and partners.

Step 3: Create your policy certificate template

- Navigate to Templates and click Create Template.

- Set the title as Policy Certificate or as you desire.

Add:

- Company logo

- Policy details (policy number, holder name, coverage summary)

- Authorised signatory

- Click Save.

Step 4: Upload the policy certificate

- Click Create Verification and upload the policy certificate in PDF format.

Step 5: Select domain and template

- Choose your custom domain.

- Select the policy certificate template you created.

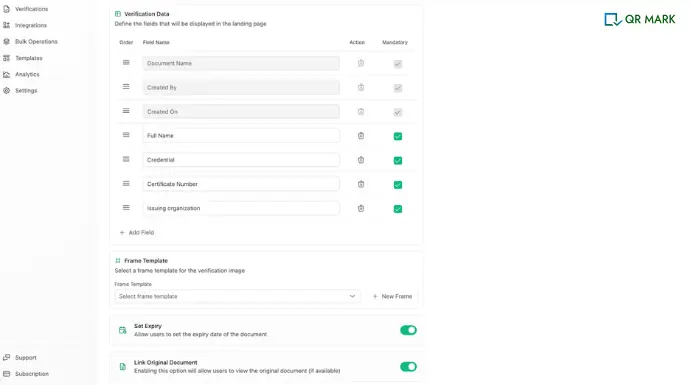

Step 6: Configure the verification record

- Name the record using the policy number or policyholder name for easy tracking.

Choose whether the verification image should appear:

- On the first page only, or

- Across all pages of the policy document

Step 7: Generate and place the verification image

- Click Generate Verification Image.

- Adjust its size and position to fit neatly within the policy certificate layout.

- Download the final secured and verifiable policy certificate PDF.

To understand how it works using add-in/add-ons in MS WORD or Google Docs – read this.

Conclusion

Insurance fraud doesn’t start at the time of claims—it starts much earlier, often at the document level. As we’ve seen, once a document leaves your system, it moves across multiple hands, and without a way to verify it instantly, it becomes vulnerable. That’s the gap fraudsters exploit.

The shift insurers need to make is simple: stop relying on trust and start enabling verification. Securing documents at the time of issuance ensures that wherever those documents go, their authenticity can be confirmed in seconds—by your team, your partners, or your customers.

Not all fraud solutions solve the same problem. The right approach depends on where your biggest risk lies. But if document-level fraud is a concern—and for most insurers, it is—then choosing a solution that works at the point of issuance gives you a clear advantage.

Because in the end, the goal isn’t just to detect fraud. It’s to make it harder to exist in the first place.

Insurance fraud doesn’t start at the claims stage.

Secure your documents at issuance — and give every verifier an instant, trustworthy way to confirm them. See how QR Mark works for your team .

Frequently asked questions

What is the most common type of insurance document fraud?

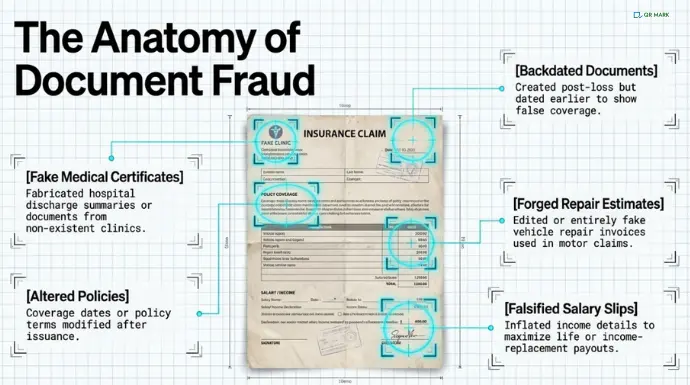

Medical certificate fraud is the most common type in health and personal accident insurance claims. This includes fabricated discharge summaries, inflated treatment bills, and certificates from non-existent or unverified healthcare providers. In motor insurance, forged or inflated repair estimates from garages are the most frequent document-level fraud pattern.

How do insurers currently verify the authenticity of claim documents?

Most insurers rely on a combination of visual inspection, direct contact with the issuing organisation (phone or email), and cross-referencing details against internal databases. This approach is slow, typically taking 24-72 hours per verification, and does not scale for high-volume claims operations. It also fails against digitally altered documents that retain genuine headers and formatting.

Does the person verifying a QR Mark document need to download an app?

No. QR Mark verification works with any standard smartphone camera. The verifier scans the QR code using their phone camera, which opens the verification page in a browser. No app download, no account creation, no friction. This is one of the reasons verifier adoption is higher with QR Mark than with tools that require a dedicated validator.

Can QR Mark be used for both digital and printed insurance documents?

Yes. The Verification Image works on both printed documents (scan the QR with a phone camera) and digital PDFs (click the verification URL embedded in the document). This matters for insurance because claim documents arrive in both formats depending on the issuer and the claimant.